Thinking of Starting a Company in 2026? Here Are Some Industries You Might Want to Consider

square.jpg)

Deciding which industry to launch a startup in isn’t just about passion or a cool idea. It’s also about funding climates, market stability, barriers to entry, regulation, tariffs, and long-term viability. As we head into 2026, the startup landscape shows clear patterns: investors are increasingly concentrating capital in sectors with structural demand and enterprise traction, while other industries face headwinds from regulation, capital scarcity, or macroeconomic pressures. This article walks founders through the most promising industries to build in 2026, and those that may pose significant challenges, so you can make an informed decision about where to place your bet.

High-Potential Industries for 2026

Several sectors stand out for their robust funding trends, growing market demand, and relative resilience against regulatory or tariff risks. These are industries where starting a company in 2026 could align with investor interest and real market needs.

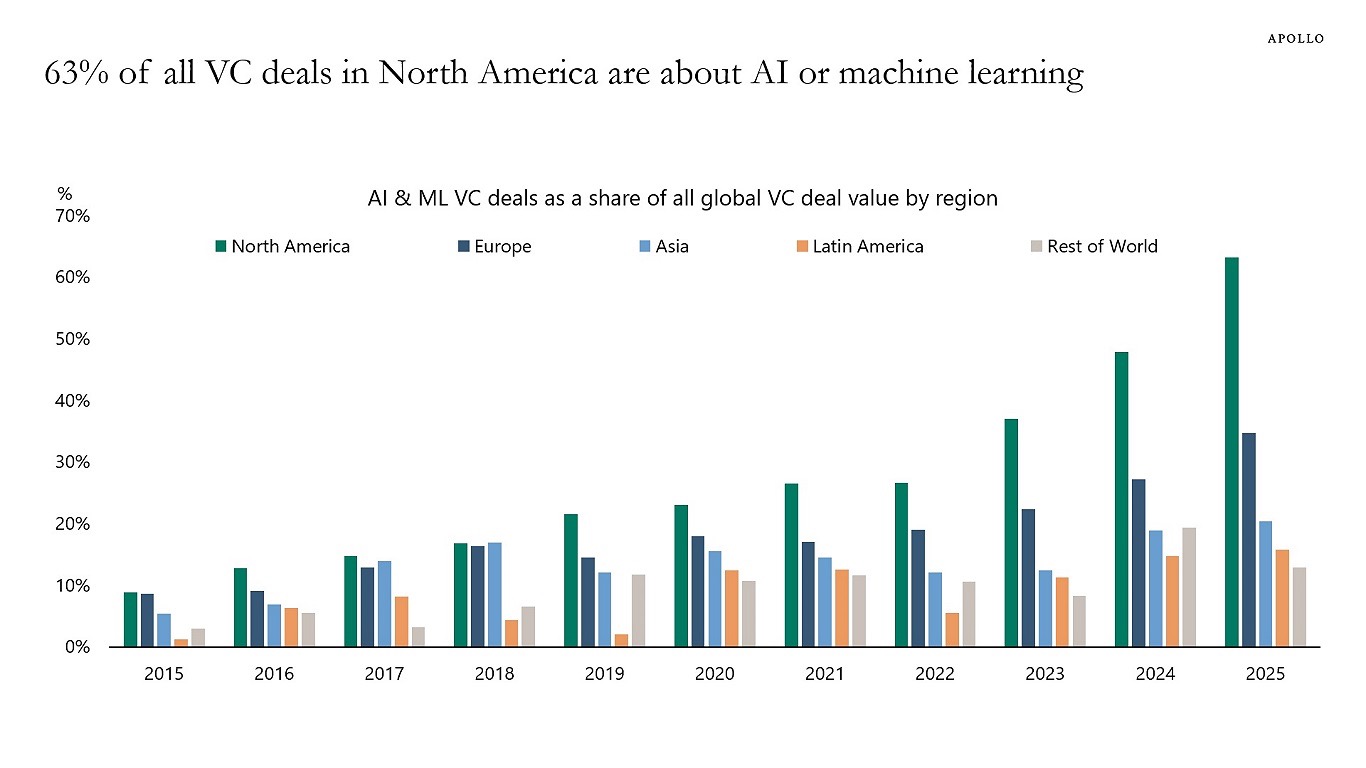

Artificial Intelligence and AI-Driven Infrastructure

The most dominant story in venture capital over the last few years has been AI. Crunchbase data shows that nearly half of all startup funding in 2025 went to AI companies, with hundreds of billions committed across the ecosystem. AI remains the top driver of venture capital investment worldwide, and this momentum is expected to carry over into 2026 as software transforms more traditional industries.

What makes AI so compelling is its versatility and scalability. Startups building AI tools for niche enterprise workflows, automation platforms, AI security, or embedded intelligence in other verticals are increasingly attractive to both VCs and strategic acquirers. The high capital intensity of foundational AI training and model deployment is balanced by extremely large addressable markets and strong revenue potential for companies that can deliver measurable productivity gains. That said, founders should be mindful of the regulatory complexity surrounding data use, privacy, and model governance as different jurisdictions grapple with AI oversight.

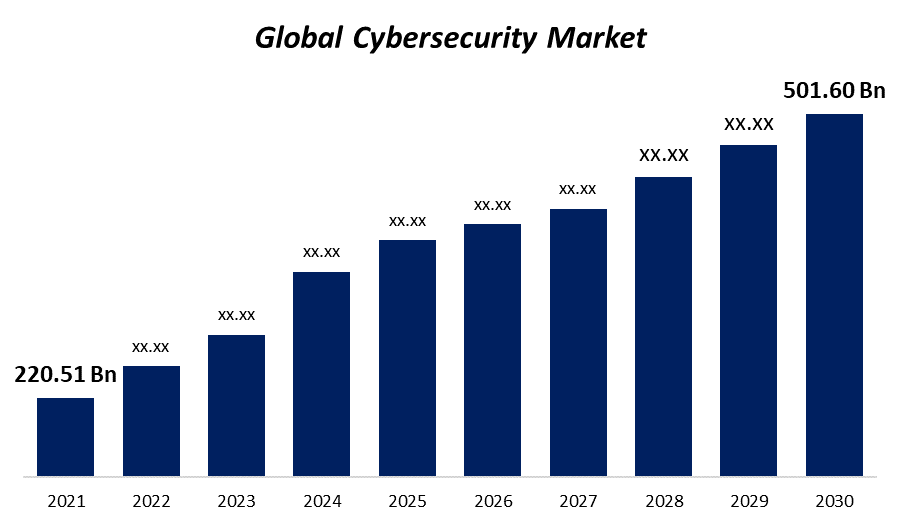

Cybersecurity and Trust Technologies

As digital transformation accelerates, so do security threats. The global cybersecurity market is projected to exceed $500 billion by 2030, driven by demand from enterprises and governments alike. Startups focused on AI-native security platforms, secure inference, model governance tools, and zero-trust architectures are particularly well positioned, since they align directly with enterprise budgets and long-term spending priorities.

Funding isn’t just large; it’s also sustained. Companies that can demonstrate real reductions in risk exposure or compliance costs tend to earn stickier customer relationships, critical for subscription-based business models. Because cybersecurity is a response to clear pain points, this industry tends to attract stable and ongoing investment, unlike some consumer sectors that fluctuate with trends.

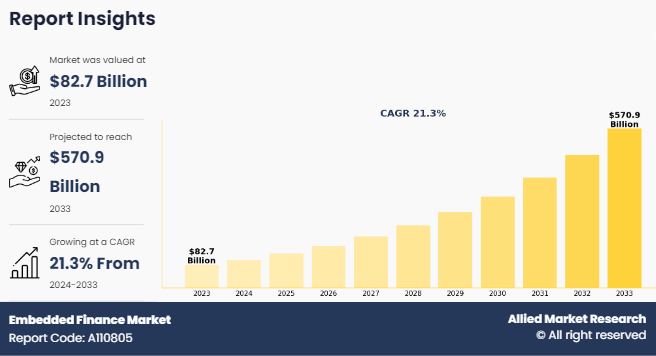

Fintech and Embedded Finance

Fintech remains a top startup category heading into 2026, with embedded finance, payments infrastructure, insurtech, and compliance-automated platforms drawing capital and customers. Funding in fintech rebounded in 2025, with billions flowing into deals across payments and financial infrastructure, marking a comeback after a period of contraction.

The biggest advantage of fintech for new founders is the breadth of sub-sectors and the diversity of entry points. Companies focused on RegTech and compliance automation tools that help other fintechs satisfy real-time AML/KYC and reporting requirements, benefit from structural demand and can often launch with smaller capital bases if they nail product-market fit. However, founders should bear in mind that more traditional banking and lending startups still face substantial regulatory barriers and capital requirements, which can slow growth and complicate fundraising.

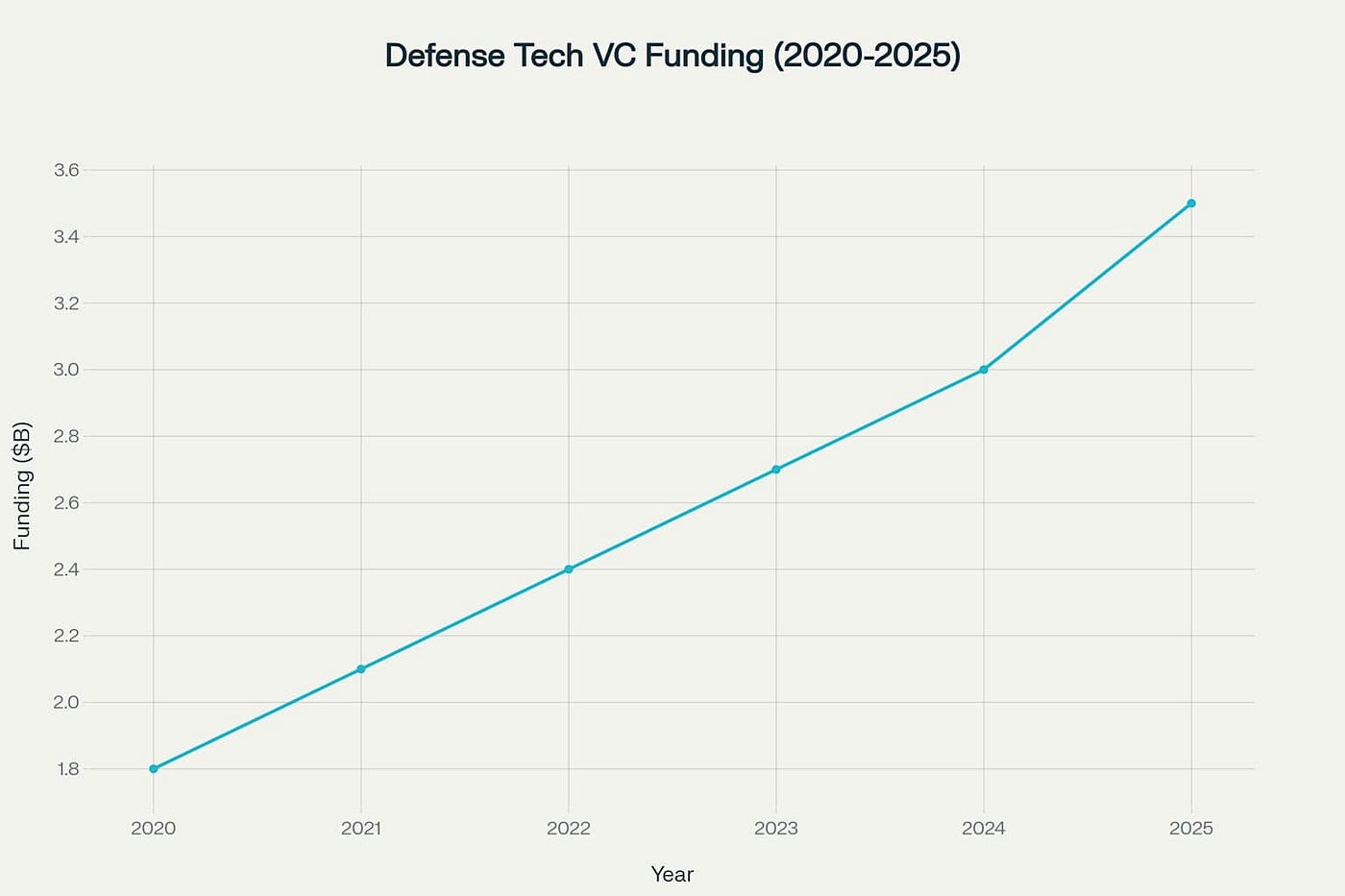

Defense and Dual-Use Technologies

The defense tech and aerospace sectors saw considerable venture interest in 2025, with billions in funding for startups building autonomous systems, AI-powered sensing, and dual-use platforms that serve both civilian and military markets. Government defense spending is projected to stay strong globally, giving startups the option of blending VC capital with government contracts, which can provide stability and longer-term revenue visibility.

That said, entrants into defense tech should be prepared for complex procurement cycles, security clearances, and geopolitical considerations that can delay commercial traction. Still, if a startup can secure strategic partnerships early, for example with prime contractors or defense agencies, the payoffs can be large compared to the initial investment, and the ecosystem remains open to innovation.

Climate and Clean Technologies

Climate tech, renewable energy, and energy transition solutions continue to attract targeted investment, even if overall funding cycles fluctuate. As governments and corporations commit to net-zero goals, areas like energy storage, grid optimization, carbon mitigation services, and industrial decarbonization are drawing significant interest. These sectors benefit not only from venture capital but also from policy incentives, grants, and infrastructure programs that can de-risk early-stage development.

For founders, the challenge in climate tech is usually capital intensity and longer timelines compared to pure software products. Hardware, emissions reduction technology, or advanced materials typically require larger upfront investment and more time to reach commercialization. But the structural tailwinds and expanding policy frameworks (e.g., production tax credits, clean energy mandates) make this an appealing space for startups willing to play the long game.

Industries Facing Headwinds in 2026

Not all sectors offer equal opportunities in 2026. Some are becoming harder to break into because of capital contraction, regulatory complexity, rising tariff pressures, or technological hurdles. Founders should approach these areas cautiously.

Healthcare and Biotech (Especially Small Molecule Focus)

The healthcare sector as a whole continues to attract investment, especially in areas like AI-powered diagnostics and digital health platforms that improve patient outcomes or operational efficiency. However, specific corners of the healthcare and biotech space, particularly small molecule drug development, face regulatory headwinds and shifting reimbursement incentives in some major markets.

Recent policy changes, such as negotiated pricing frameworks under the U.S. Inflation Reduction Act, are expected to compress margins and shift investment away from certain drug classes, and tariffs on imported pharmaceuticals could further impact profitability for companies without domestic manufacturing. For founders without deep expertise and substantial capital to navigate development timelines and regulatory pathways, this is one of the tougher startup environments.

Deep Hardware and Consumer Goods

Consumer hardware and durable goods startups can struggle due to the economics of inventory, tariffs, and supply chain friction. While not inherently doomed, these startups face higher barriers to entry and smaller margins compared to software or platform businesses. Inventory risk increases sharply when demand forecasts are uncertain, and tariffs can erode pricing power in critical markets.

For example, the growth of hardware startups often slows or stalls when geopolitical tariffs or raw material costs rise, pushing founders into capital-intensive cycles just to keep operating. Unless the product solves a very specific and high-value problem with defensible advantages, it can be difficult to compete with established manufacturers and lower-cost producers.

Emerging Consumer Sectors Without Structural Tailwinds

While lifestyle businesses and consumer-oriented services (like e-commerce or VR/AR applications) can find niches, they generally do not enjoy the structural funding tailwinds available to sectors like AI, cybersecurity, or fintech infrastructure. Unless a startup in this space can innovate around a clear inefficiency or unmet need, it may struggle to attract serious venture capital in an era where investors prefer scalable, defensible tech platforms.

Why These Trends Matter

The industries that look strongest for 2026 all share a few common traits that matter to founders and investors alike:

- Scalable Demand, Not Trendiness: Markets where customers have recurring or mission-critical needs, like security, finance operations, or energy transition, tend to budget for long-term solutions. These markets are less prone to hype cycles and more likely to fund ventures that promise sustainable revenue.

- Capital Efficiency and Clear Value Delivery: Sectors where early revenues can validate product-market fit, for example, embedded finance platforms or cybersecurity tools, are easier to fund on sensible terms. Heavy hardware or long R&D cycles require far more capital and patience, which smaller founders may lack.

- Regulatory and Tariff Awareness: Industries entangled with regulation or trade barriers need founders who understand those landscapes deeply. Compliance isn’t an afterthought; in fintech and healthcare especially, it’s a core part of the business model that can dictate customer acquisition and retention.

- Policy and Macro Tailwinds: Governments around the world are directing capital toward clean energy, digital infrastructure, and national security technologies, which can help startups secure both public and private funding. Aligning your business model with these policy priorities can give you both credibility and leverage in fundraising.

Conclusion

Choosing the right industry to start a company in 2026 is as much about market fundamentals as it is about innovation. AI and cybersecurity remain at the top of the list for founders seeking deep funding pools and scalable business models. Fintech and climate tech offer structural opportunities but require strong execution and, in some cases, regulatory savvy. Defense and aerospace might pay off handsomely for the right team, but they bring complex procurement and competition dynamics. Meanwhile, deeply hardware-based or lightly differentiated consumer ventures face tougher capital environments and margin pressures.

Your startup idea’s success will be shaped not only by your vision but by how well it aligns with these larger dynamics. By understanding where venture capital is flowing, and where it’s receding, you stand a better chance of building something that thrives in 2026 and beyond.

Read - The Top 5 Best and Worst Startup Investments of 2025 and What They Reveal About Venture Capital

Weekly

Newsletter.